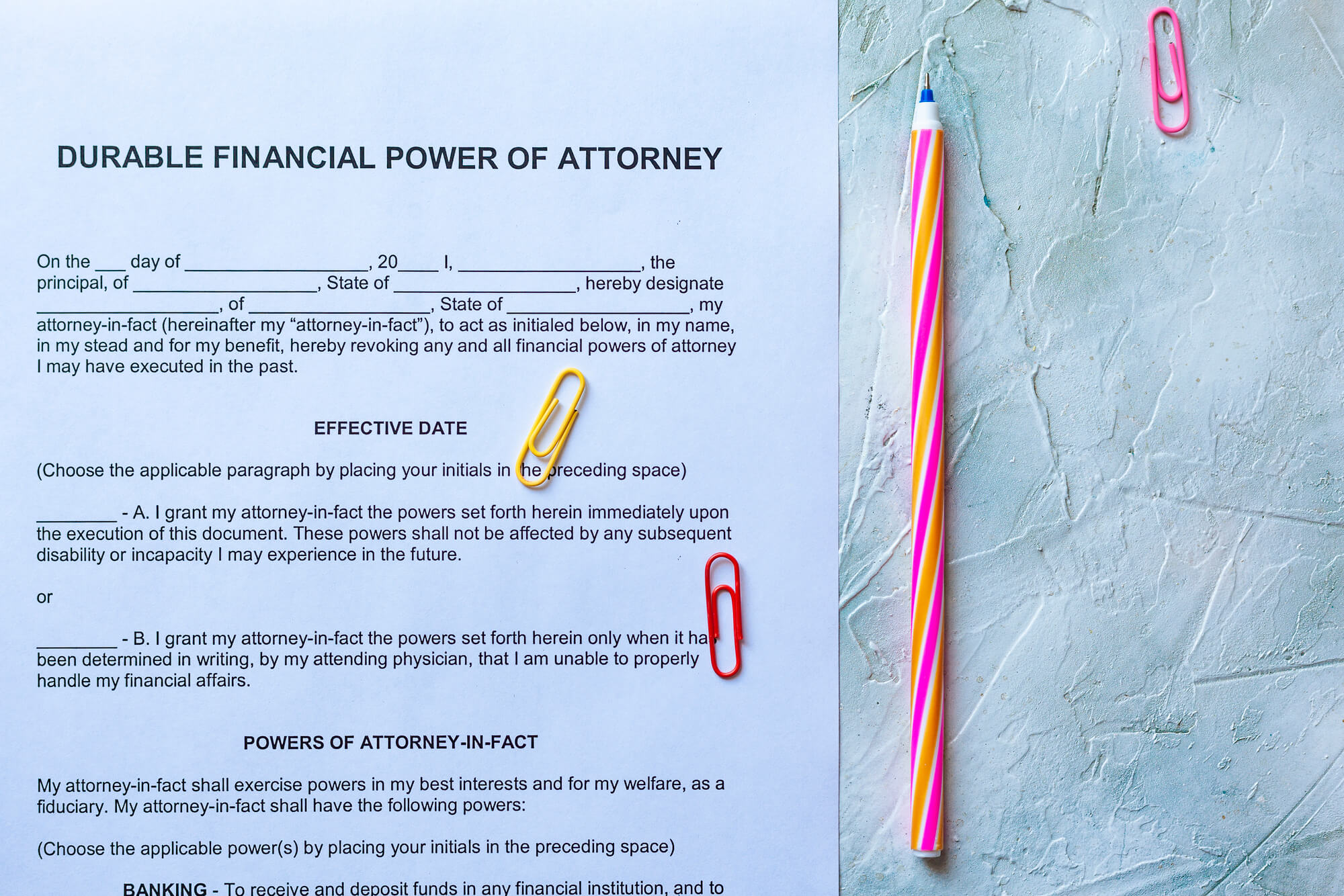

In the intricate web of financial planning, individuals often focus on accumulating wealth, investments, and retirement funds. While these aspects are crucial, one essential component that is sometimes overlooked is establishing a Financial Power of Attorney (FPOA). This legal document can play a pivotal role in safeguarding your financial interests and ensuring a smooth transition of decision-making powers when needed.

Understanding Financial Power of Attorney

A Financial Power of Attorney is a legal document that grants a trusted individual, known as the agent or attorney-in-fact, the authority to manage your financial affairs in the event you become unable to do so. This incapacity may arise due to various reasons, including illness, injury, or other unforeseen circumstances.

The Risks of Procrastination

1. Financial Vulnerability:

Without an FPOA, your financial affairs could be left hanging in the balance during a period of incapacity. This vulnerability could lead to missed bill payments, delayed financial transactions, and overall mismanagement of your assets.2. Legal Complications:

In the absence of an FPOA, your loved ones may need to pursue legal avenues such as guardianship or conservatorship to gain control over your financial matters. These processes are not only time-consuming but can also be emotionally and financially draining.3. Limited Decision-Making Control:

Without a designated agent, important financial decisions, such as managing investments, selling or purchasing real estate, or handling tax matters, may be subject to court approval rather than your specific preferences.The Role of the Financial Power of Attorney

1. Continuity of Financial Management:

An FPOA ensures the seamless continuation of your financial management in case of your incapacity. Your chosen agent can step in immediately, paying bills, managing investments, and handling day-to-day financial responsibilities.2. Personalized Decision Making:

By designating a specific individual as your agent, you retain control over who manages your financial affairs. This person should be someone you trust implicitly, ensuring that your financial decisions align with your values and preferences.3. Preventing Family Disputes:

Clearly outlining your wishes through an FPOA can help prevent family disputes that may arise in the absence of explicit instructions. This legal document acts as a roadmap for your financial decisions when you are unable to communicate them yourself.Navigating the Process of Establishing an FPOA

1. Choosing the Right Agent:

Carefully consider who you want to entrust with your financial affairs. This person should be not only trustworthy but also financially savvy and responsible. It could be a family member, friend, or even a professional advisor.2. Legal Assistance:

While it is possible to create a basic FPOA using templates, seeking legal advice is highly recommended. An attorney can help you customize the document to your specific needs, ensuring it complies with state laws.3. Regular Review:

Life circumstances change, and so should your FPOA. Regularly review and, if necessary, update the document to reflect changes in your relationships, financial situation, or preferences.Conclusion

In the intricate dance of financial planning, the Financial Power of Attorney is a crucial partner, ensuring that your affairs are managed according to your wishes even when you can't orchestrate them yourself. The dangers of not having an FPOA are real and can significantly impact your financial well-being and that of your loved ones. Take the proactive step of establishing a robust Financial Power of Attorney, and you'll be fortifying your financial future against unforeseen challenges. Remember, it's not just about wealth accumulation; it's about wisely protecting and preserving what you've worked so hard to build.